Chapter 6 — Avoiding Medicare Penalties

How to keep your hard-earned dollars instead of paying Uncle Sam for life

1. Why Medicare Penalties Exist (And Why They’re So Brutal)

Let me start with a story that illustrates exactly what my team and I see regularly. After nearly 20 years in the Medicare industry, now specializing exclusively with veterans, I’ve seen this costly mistake too many times. A Navy veteran had delayed enrolling in Medicare Part B for three years because he thought his VA coverage was sufficient. When he finally came to us, he was facing a 30% lifetime penalty on his Part B premium.

Instead of paying the standard $185 monthly, he now pays $240.50 every month for 2025. This includes the 30% penalty. What makes this penalty especially brutal is that it’s calculated as a percentage of the current year’s Part B premium, not a fixed dollar amount. This means as Medicare premiums rise every year, your penalty grows right along with them. This penalty lasts for the rest of his life. Over 20 years, that’s at least an extra $13,320, assuming the Part B premium never increases. But we know it will increase, making the actual cost much higher.

Congress didn’t create Medicare penalties to be cruel. They created them to prevent what insurance companies call “adverse selection.” Without penalties, healthy people would wait until they got sick to enroll in Medicare, leaving only the sickest people in the program. This would drive costs through the roof for everyone.

The penalty system creates a powerful incentive. Enroll when you’re supposed to, and you pay standard rates. Wait until you’re sick, and you pay extra for the rest of your life. It’s harsh, but it keeps the entire Medicare system as financially stable as possible.

The Three Types of Medicare Penalties:

- Part B Late Enrollment Penalty: 10% per year you delay, permanent

- Part D Late Enrollment Penalty: 1% per month you delay, permanent

- Part A Late Enrollment Penalty: 10% for twice the delay period (only affects those who must buy Part A)

For veterans, the Part B penalty is by far the most dangerous because VA benefits are not creditable coverage for Medicare Part B, meaning you can’t use VA healthcare to justify delaying Medicare enrollment.

This is often confused with VA drug coverage, which is creditable for Part D penalties. VA and TRICARE for Life prescription coverage protects you from Part D penalties, but they do not protect you from Part B penalties. During my extensive time helping veterans navigate Medicare, this confusion between VA drug coverage being creditable and VA medical coverage not being creditable has cost more veterans money than almost any other misconception.

2. The Part B Penalty: Simple Math, Devastating Results

The Part B late enrollment penalty is brutally simple to calculate but devastating in its long-term impact. Throughout my Medicare career working with veterans, I’ve seen how this simple formula can cost tens of thousands of dollars.

The Formula:

- 10% penalty for every full 12-month period you delay enrollment

- Applied to the current year’s Part B premium (not a fixed dollar amount)

- The penalty lasts for as long as you have Medicare Part B, typically for life

As I explained earlier, your penalty grows every year along with Medicare premiums. Let me show you what this means using conservative projections.

If You Should Enroll in 2025 But Delay 3 Years Until 2028:

- 2025: You miss enrollment (standard premium $185)

- 2028: You finally enroll with 30% penalty. Your premium: $276.80 (penalty: $63.88)

- 2030: Your premium grows to $350.70 (penalty: $116.90)

The Compounding Effect: Assuming just a 4.8% annual increase in Part B premiums, your penalty burden grows significantly:

- 1 year delay (10% penalty): Start paying $19.39 extra monthly, grows to $23+ by 2030

- 3 years delay (30% penalty): Start paying $63.88 extra monthly, grows to $117+ by 2030

- 5 years delay (50% penalty): Start paying $116.90 extra monthly, grows to $175+ by 2030

A 3-year delay from your 2025 enrollment date doesn’t just cost you $64 extra per month initially. That penalty grows every single year for the rest of your life. Looking at the projections, a veteran who delays 3 years will pay over $89 monthly in penalties by 2029 and over $116 by 2030.

Over 20 years, you’re looking at paying at least $20,000-$25,000 extra in penalties alone, and that’s assuming premium increases stay modest at 4.8% annually. For veterans on fixed incomes combining Social Security and military retirement, this unnecessary expense can significantly impact retirement security.

Year Enrolled | Years Delayed | Estimated Part B Premium | Penalty (10% per year) | Total Monthly Premium |

2025 | 0 | $185.00 | $0 | $185.00 |

2026 | 1 | $193.88 | $19.39 | $213.27 |

2027 | 2 | $203.18 | $40.64 | $243.82 |

2028 | 3 | $212.92 | $63.88 | $276.80 |

2029 | 4 | $223.12 | $89.25 | $312.37 |

2030 | 5 | $233.80 | $116.90 | $350.70 |

3. The Dangerous Myth: “VA Coverage Protects Me”

During my extensive Medicare career, now dedicated entirely to veterans, I’ve discovered that this single misunderstanding costs more money than almost any other Medicare mistake. Unlike group health insurance through a large employer, VA benefits are not creditable coverage for Medicare purposes.

The Social Security Administration recognizes specific types of creditable coverage that allow you to delay Part B without penalty:

Approved Creditable Coverage:

- ✓ Employer group health plan with 20+ employees (while actively working)

- ✓ Federal Employees Health Benefits (FEHB) (while actively working; retirees must enroll in Part B to avoid penalties)

- ✓ A spouse’s large employer coverage (while they’re actively working)

- ✓ Some union health plans with specific characteristics

NOT Creditable Coverage:

- ✗ VA health care (all types and priority groups)

- ✗ VA Community Care

- ✗ CHAMPVA

- ✗ COBRA coverage

- ✗ Most retiree health plans

- ✗ Individual/private insurance policies

- ✗ Medicaid

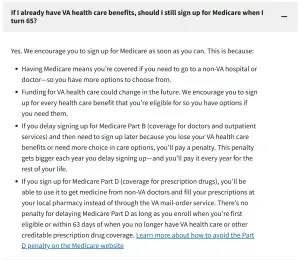

The VA’s Own Warning: “Yes. We encourage you to sign up for Medicare as soon as you can. This is because:

- Having Medicare means you’re covered if you need to go to a non-VA hospital or doctor, so you have more options to choose from.

- Funding for VA health care could change in the future. We encourage you to sign up for every health care benefit that you’re eligible for so you have options if you need them.

- If you delay signing up for Medicare Part B (coverage for doctors and outpatient services) and then need to sign up later because you lose your VA health care benefits or need more choice in care options, you’ll pay a penalty.”

(Source: VA.gov, https://www.va.gov/health-care/about-va-health-benefits/va-health-care-and-other-insurance/)

We share this VA warning with every veteran we work with because it comes directly from the source. The VA itself is telling you that their coverage alone isn’t enough.

Even the VA knows their coverage doesn’t protect you from Medicare penalties. Yet thousands of veterans delay enrollment every year because they receive advice from professionals who may not specialize in the unique intersection of military and Medicare benefits.

4. TRICARE for Life: The Double Penalty Trap

If you’re a military retiree with TRICARE for Life, the penalty situation becomes even more severe.

The TRICARE for Life Double Penalty:

- You lose TRICARE for Life immediately if you don’t have Medicare Parts A and B

- You face the Part B late enrollment penalty when you finally do enroll

Throughout my years helping military retirees navigate Medicare, I’ve seen this double penalty trap repeatedly. Consider a career military officer who retired after 24 years of service at age 44. She had excellent TRICARE coverage and figured she didn’t need Medicare when she turned 65. She delayed enrollment for four years, thinking TRICARE was sufficient.

At age 69, when she finally tried to enroll after her heart attack, she discovered:

- Her TRICARE for Life had been suspended for four years

- She owed a 40% late enrollment penalty on Part B

- Her monthly Part B premium jumped from $185 to $259

The cost of her mistake:

- Four years without TFL coverage during a medical emergency

- Extra $74/month for the rest of her life ($17,760 over 20 years if premiums never increased)

- But that’s the minimum: with typical 4.8% annual premium increases, her penalty could exceed $25,000 over 20 years

- Plus the stress and financial burden of uncovered medical bills during her heart attack

Remember, that 40% penalty grows every year as Medicare premiums increase, making it even more painful over time.

This example isn’t unique. We’ve worked with numerous military retirees who faced similar situations because they didn’t understand that TRICARE for Life absolutely requires Medicare Parts A and B.

When working with military retirees, we always emphasize there are no exceptions to the Medicare requirement for TRICARE for Life. Federal law doesn’t bend, regardless of your rank, years of service, or other circumstances.

Federal law (10 U.S.C. § 1086(d)) and regulation 32 CFR § 199.17 specifically require both Medicare Parts A and B for TRICARE for Life eligibility. The regulation is crystal clear: “when a retiree or retiree family member becomes individually eligible for Medicare Part A and enrolls in Medicare Part B, he/she is automatically eligible for TRICARE-for-Life” (Source: 32 CFR § 199.17, https://www.law.cornell.edu/cfr/text/32/199.17).

TRICARE’s own website confirms: “If you have Medicare Part A, you must also have Medicare Part B to remain eligible for TRICARE” (Source: TRICARE.mil, https://tricare.mil/Plans/Eligibility/MedicareEligible).

5. Your Personal Penalty Timeline: Critical Dates Every Veteran Must Know

Understanding exactly when you must enroll is crucial for avoiding penalties. In my years helping veterans, I’ve seen too many costly mistakes that could have been avoided with proper timing.

Initial Enrollment Period (IEP): Your Penalty-Free Window

- Begins: 3 months before the month you turn 65

- Ends: 3 months after the month you turn 65

- Total window: 7 months (3 months before + your 65th birthday month + 3 months after)

- Best practice: Enroll the first week you are eligible. Medicare becomes effective the first day of your 65th birthday month. Exception: If you were born on the 1st of the month, your Medicare and TRICARE for Life become effective a month early.

The 1st of the month rule is really important. Many people don’t know about this exception!

The Centers for Medicare & Medicaid Services confirms: “If your birthday is on the first of the month, coverage starts the month before you turn 65” (Source: Medicare.gov, https://www.medicare.gov/basics/get-started-with-medicare/sign-up/when-does-medicare-coverage-start).

Example Timeline for June Birthday:

- March-May (age 64): First 3 months of IEP. Coverage starts June 1st

- June (turning 65): Birthday month. Coverage starts July 1st if you enroll this month

- July-September (age 65): Last 3 months of IEP. Coverage delayed until month after enrollment

CMS officially defines the IEP as “a 7-month period that begins 3 months before the month a person turns 65, their birthday month and ends 3 months after the person turns 65” (Source: CMS.gov, https://www.cms.gov/medicare/enrollment-renewal/original-part-a-b).

Special Enrollment Period (SEP): The Exception for Active Workers

- Available only if you have creditable employer coverage (20+ employee group plan)

- Lasts 8 months after your employment ends OR your creditable coverage ends

- Critical: You must be actively working, not just receiving retiree benefits

Medicare.gov confirms: “Your 8-month Special Enrollment Period to sign up for Part B starts when you stop working, even if you choose COBRA or other coverage that’s not Medicare” (Source: Medicare.gov, https://www.medicare.gov/basics/get-started-with-medicare/medicare-basics/working-past-65/).

General Enrollment Period (GEP): Last Resort

- January 1 – March 31 each year

- Coverage starts the 1st of the month after your enrollment

- Late enrollment penalties highly likely to apply

According to the Social Security Administration: “This is the ‘General Enrollment Period,’ and there is typically a life-long penalty if you sign up during this time” (Source: SSA.gov, https://www.ssa.gov/medicare/plan/when-to-sign-up).

Most veterans who are not currently working full time and receiving medical benefits from their employer should enroll during their Initial Enrollment Period to avoid any penalty risk. We regularly work with veterans who could have avoided penalties entirely by understanding these critical timelines.

Disclaimer: Still working with employer health benefits? Contact your HR department or group health administrator immediately to verify if your coverage is creditable for Medicare purposes. Don’t assume anything. Verify your specific situation to avoid costly penalties.

6. The Specialist Difference in Penalty Prevention

Working with veteran Medicare specialists like my team makes a crucial difference. My extensive Medicare background combined with our sole focus on veteran situations allows us to catch details that others might overlook.

What Generic Advisors and Well-Meaning Professionals Often Miss:

- They may assume VA coverage is creditable (it’s not)

- They might not fully understand TRICARE for Life requirements

- They may not know about veteran-specific enrollment rules

- They often provide one-size-fits-all advice

It’s important to note that VA and TRICARE employees are experts in their own systems, but they aren’t Medicare specialists. They provide valuable guidance within their areas of expertise, but Medicare integration requires specialized knowledge.

What Veteran Medicare Specialists Do Differently:

- We understand that VA coverage doesn’t protect from penalties

- We know the TRICARE for Life integration requirements

- We help veterans time their enrollment perfectly

- We provide strategies specific to military situations

The Centers for Medicare & Medicaid Services clearly states that for enrollments after your Initial Enrollment Period, “months where you had group health plan coverage are excluded from the LEP calculation” but VA coverage is not considered group health plan coverage (Source: CMS.gov, https://www.cms.gov/medicare/enrollment-renewal/original-part-a-b).

Medicare.gov confirms this critical distinction: “It’s important to sign up for Medicare coverage during your Initial Enrollment Period, unless you have other coverage that’s similar in value to Medicare (like from an employer)” – and VA coverage does not qualify as this type of creditable coverage (Source: Medicare.gov, https://www.medicare.gov/basics/costs/medicare-costs/avoid-penalties).

Even the VA itself acknowledges this on their official website: “If you delay signing up for Medicare Part B (coverage for doctors and outpatient services) and then need to sign up later because you lose your VA health care benefits or need more choice in care options, you’ll pay a penalty” (Source: VA.gov, https://www.va.gov/health-care/about-va-health-benefits/va-health-care-and-other-insurance/).

Real Example: Penalty Prevention Success

This situation happens more often than you’d think. A veteran approaching 65 was told by an advisor that he could delay Medicare Part B without penalty because of his VA coverage. Fortunately, something didn’t feel right to him about this advice. When he contacted my team six months before his birthday, we immediately corrected this dangerous misinformation and helped him enroll during his Initial Enrollment Period.

The result: He avoided what would have been at least an $18.50 monthly penalty, not including Part B premium increases for the rest of his life. Over 20 years, proper guidance saved him at least $4,440.

This demonstrates why working with specialists who focus only on veteran Medicare issues matters so much. We’ve seen these situations countless times and know exactly how to protect veterans from costly mistakes.

7. How to Appeal a Medicare Penalty (When the System Makes Mistakes)

Sometimes the Social Security Administration makes errors in penalty assessments. If you believe you’ve been incorrectly charged a late enrollment penalty, you can appeal. I’ve seen successful appeals save veterans thousands of dollars, but you need to know the process and act quickly.

The Appeals Process

You’ll need to complete Form CMS-L564 (Request for Employment Information) to document your creditable coverage. This form is available at the Social Security Administration website (Source: CMS.gov, https://www.cms.gov/medicare/cms-forms/cms-forms/cms-forms-items/cms009718).

Important timing: While there’s no specific deadline for appealing a Part B penalty, you should appeal as soon as possible after receiving the penalty notice. The longer you wait, the more penalty payments you’ll make before potentially receiving a refund.

Common Successful Appeal Scenarios:

- You had creditable employer coverage but SSA didn’t recognize it

- You received incorrect information from an employer or government agency

- You were affected by a natural disaster or other exceptional circumstances

- There were processing delays that weren’t your fault

What You Need for a Successful Appeal:

- Form CMS-L564 (Request for Employment Information)

- Letter from employer confirming you had creditable coverage

- Pay stubs or benefits statements showing coverage dates

- Documentation of any misinformation you received

Success Story: The Appeal That Saved $12,000

An Air Force veteran was incorrectly charged a 20% Part B penalty when he enrolled at age 67. He had been working for a federal contractor with creditable coverage, but SSA didn’t have proper documentation. We advised him to complete Form CMS-L564 with a letter from his HR department.

The result: The appeal was successful, eliminating the penalty and providing a $1,200 refund for penalties already paid. Over his lifetime, this appeal saved him approximately $12,000.

When we work with veterans who face penalty issues, we don’t just help them understand the penalties. We help them fight incorrect assessments and win.

Additional Rights You Should Know

If your initial appeal is denied, you have reconsideration rights. The Medicare appeals process includes multiple levels:

- Reconsideration by Social Security Administration

- Hearing before an Administrative Law Judge if needed

- Appeals Council review if necessary

- Federal Court review as a final option

Most successful penalty appeals are resolved at the first or second level when proper documentation is provided. Veterans who gather complete and compelling documentation often turn denials into approvals at these early stages.”

8. The Part D Penalty (Different Rules for Veterans)

Unlike Part B, VA and TRICARE for Life prescription drug coverage IS considered creditable coverage for Medicare Part D purposes. This distinction saves most veterans from Part D penalties entirely.

Medicare.gov specifically confirms: “Creditable prescription drug coverage is prescription drug coverage that’s expected to pay, on average, at least as much as Medicare drug coverage. This could include drug coverage from a current or former employer or union, TRICARE, the Indian Health Service, or the Department of Veterans Affairs (VA)” (Source: Medicare.gov, https://www.medicare.gov/health-drug-plans/part-d/basics/creditable-coverage).

If you have VA or TRICARE for Life drug coverage:

- You can delay Medicare Part D enrollment without penalty

- You must maintain continuous drug coverage to stay protected

- If you lose VA or TRICARE drug coverage, you have 63 days to enroll in Part D without penalty

The VA website confirms: “There’s no penalty for delaying Medicare Part D as long as you enroll when you’re first eligible or within 63 days of when you no longer have VA health care or other creditable prescription drug coverage” (Source: VA.gov, https://www.va.gov/health-care/about-va-health-benefits/va-health-care-and-other-insurance/).

The Part D penalty calculation:

- 1% of the “national base beneficiary premium” ($36.78 in 2025) times the number of full, uncovered months

- Added to your premium for as long as you have Medicare drug coverage

Example: 14 months without creditable coverage = 14% × $36.78 = $5.15 monthly penalty (rounded to $5.20), lasting for as long as you have Part D coverage

Why This Matters for Veterans

The good news is that VA drug coverage protects most veterans from Part D penalties, unlike the Part B situation where VA coverage provides no protection. However, you should keep documentation of your VA drug coverage in case you ever need to prove it was creditable.

We always verify your prescription drug coverage status to ensure you are protected from unnecessary penalties. Many veterans don’t realize they need to maintain continuous coverage. If you drop VA enrollment or lose TRICARE benefits, that 63-day window to get Part D coverage becomes critical.

Important Note About Verification

If you ever join a Medicare drug plan, it may send you a letter asking if you had creditable prescription drug coverage. Keep your VA enrollment verification or TRICARE documentation to prove your coverage was creditable. This simple step can prevent penalty disputes later.

9. IRMAA: The Additional Surcharge That Catches Veterans Off Guard

Before we wrap up penalties, I need to mention another cost that catches many veterans by surprise: Income Related Monthly Adjustment Amount (IRMAA). While technically not a “penalty,” IRMAA is an additional surcharge that can significantly increase your Medicare costs if you’re not prepared for it.

IRMAA affects veterans whose modified adjusted gross income (MAGI) from two years prior exceeds certain thresholds. For 2025 premiums, they’re looking at your 2023 income. This two-year lookback often catches veterans off guard, especially those who had high-income years before retirement.

2025 IRMAA Impact (Examples):

- First bracket: Income $106,001-$133,000 (single) → Pay $259/month instead of $185

- Second bracket: Income $133,001-$167,000 (single) → Pay $370/month instead of $185

- Highest bracket: Income $500,000+ (single) → Pay $628.90/month instead of $185

Common IRMAA Triggers for Veterans:

- Large pension lump-sum distributions

- Significant Roth IRA conversions

- Capital gains from property sales

The Good News:

Many veterans don’t realize this appeals process exists, but it can save thousands annually. You can appeal IRMAA surcharges if your income has dropped due to retirement, job loss, divorce, or other life-changing events using Form SSA-44 (Source: SSA.gov, https://www.ssa.gov/forms/ssa-44.pdf).

This is another area where veteran specialists provide valuable guidance that generic Medicare advisors often overlook entirely. For more detailed IRMAA information specific to veterans, visit our resource page at https://veteransadvantagefinancial.vet/irmaa/

10. State Programs That Can Help with Penalties

If you’re facing Medicare penalties and have limited income, several programs can provide assistance. Based on our experience working with veterans, we need to be honest: most don’t qualify for these programs because Social Security benefits combined with veterans disability compensation or military pensions typically exceed the income limits. However, for the smaller percentage of veterans who might qualify, these programs can provide significant relief.

Medicare Savings Programs (MSPs)

These state-run programs can help pay Medicare premiums and penalties for lower-income individuals. For 2025, here are the income limits:

Program | Individual Monthly Income | Married Couple Monthly Income |

QMB | $1,325 | $1,783 |

SLMB | $1,585 | $2,135 |

QI | $1,781 | $2,400 |

Asset limits: $9,660 for individuals, $14,470 for married couples

What Each Program Covers:

- QMB: Part A and B premiums, deductibles, coinsurance, and copayments

- SLMB: Part B premium only

- QI: Part B premium only (limited funding, first-come first-served)

Extra Help (Low-Income Subsidy)

This federal program helps with Part D prescription drug costs and eliminates Part D late enrollment penalties for qualifying individuals.

2025 Income Limits:

- Individual: Up to $1,976 monthly ($23,712 annually)

- Married couple: Up to $2,664 monthly ($31,968 annually)

How to Apply:

While these assistance programs exist for veterans facing financial hardship, they fall outside our area of specialization. For qualification questions and application assistance with Medicare Savings Programs or Extra Help, contact your State Health Insurance Assistance Program (SHIP) at 1-800-MEDICARE, your local Medicaid office, or visit ssa.gov. These agencies have the specific expertise to guide you through these state and federal assistance programs.

11. Key Takeaways for Veterans

✓ VA health coverage is NOT creditable coverage for Medicare Part B—you must enroll on time regardless of your VA benefits. This is one of the most dangerous misconceptions that costs veterans thousands.

✓ Part B penalties are 10% per year of delay and last for life—a 5-year delay means you’ll pay a 50% penalty forever, potentially costing tens of thousands over retirement.

✓ TRICARE for Life users face double jeopardy—they lose TFL benefits AND face Part B penalties for delays. There are no exceptions to this federal requirement.

✓ VA prescription coverage IS creditable for Medicare Part D—but only for prescription drugs, not medical coverage. Don’t confuse these two different penalty protections.

✓ Appeals are possible with proper documentation—incorrect penalties can be overturned when you know the process.

✓ Veteran specialists understand the penalty rules better than generic Medicare advisors—we work with these situations daily, not occasionally.

✓ The cost of penalties far exceeds the cost of proper guidance—when in doubt, get veteran-specific advice from specialists who understand your unique situation.

12. What’s Coming Next

You now understand how to avoid the most costly Medicare mistakes that can drain thousands from your retirement income. The penalties we’ve discussed are completely preventable when you work with specialists who understand veteran-specific Medicare rules.

In Chapter 7, we’ll reveal the most expensive mistakes veterans make with Medicare. You’ll discover costly errors like military retirees wasting thousands on unnecessary Medigap coverage when they already have TRICARE for Life, ignoring IRMAA appeals that could save $21,000 or more, and avoiding Medicare Advantage due to outdated misconceptions that prevent them from accessing strategies to ensure they’re not overpaying for Part B.

You’ll also learn the warning signs that indicate you’re getting generic Medicare advice instead of veteran-specialized guidance. Armed with this knowledge, you’ll be able to spot these financial traps before they cost you money and make Medicare decisions that protect every dollar of your hard-earned retirement income.

Ready to protect yourself from costly Medicare penalties? My team and I specialize in penalty prevention. Call us at 888-960-8387 (VETS). Experience what WE SPEAK VETERAN™ really means.