Chapter 1 — Medicare Basics for Veterans

Everything you need to know to get started

1. Medicare at a Glance—What It Really Means for Veterans

Let’s start with the basics, but from a veteran’s perspective. You’ve navigated complex military systems throughout your career. Medicare should be no different once you understand how it works specifically for veterans.

Medicare is the federal health insurance program for Americans age 65 and older, plus some younger people with specific disabilities. But most generic Medicare guides won’t tell you that for veterans, Medicare isn’t just another insurance option. It’s often the keystone that holds your entire healthcare strategy together.

When you enroll in Medicare, it generally becomes the primary payer for medical services you receive outside the VA system. This means Medicare pays first, and other coverage like TRICARE for Life kicks in afterward (Source: TRICARE.mil, https://tricare.mil/Plans/HealthPlans/TFL). If you only have VA health benefits and no Medicare coverage, you cannot receive care outside the VA system unless the VA pre-authorizes it through their Community Care program, and they can deny those requests.

The VA itself encourages you to sign up for Medicare as backup coverage. In fact, the VA explicitly states on their website:

As you can see, the VA explicitly states they encourage veterans to sign up for Medicare because “Funding for VA health care could change in the future” and having Medicare means “you’re covered if you need to go to a non-VA hospital or doctor—so you have more options to choose from” (Source: VA.gov, https://www.va.gov/health-care/about-va-health-benefits/va-health-care-and-other-insurance/).

If you’re a military retiree, Medicare Parts A and B aren’t optional. They’re mandatory for keeping your TRICARE for Life benefits.

Think of it this way: Medicare is like the foundation of a house. Your VA benefits, TRICARE for Life, and other military health benefits are the rooms built on top of that foundation. Without a solid Medicare foundation, the whole structure becomes unstable.

Now, if you’re like my dad and use the VA for 95% of your health services, you might think of the VA as your primary foundation. But Medicare is still that critical backup structure, ready when the VA falls short. On more than one occasion, the VA has denied my father coverage. He didn’t panic because he had Medicare as his backup plan.

This layered approach isn’t just smart. It’s required. Why does this matter so much? Because life happens. Sometimes the closest VA facility is hours away. Maybe you need to see a specialist who’s not available through the VA, and the VA denies your Community Care referral.

Veterans must meet strict eligibility requirements for Community Care, including specific drive time and wait time standards, and the VA can deny requests that don’t meet their criteria. If your request is denied, you can appeal through the VA’s Clinical Appeals process, but that takes time you might not have when you need medical care (Source: VA.gov, https://www.va.gov/resources/eligibility-for-community-care-outside-va/). With Medicare as your backup, you have immediate access to civilian specialists without waiting for VA approval or appeals.

Perhaps you’re traveling and a medical emergency strikes. While the VA encourages veterans to seek immediate care without delay, they can only cover the cost of your emergency care if you meet specific requirements: you must be enrolled in VA healthcare, a VA facility wasn’t “feasibly available,” you must notify the VA within 72 hours of when your emergency care starts, and you must meet other situation-specific requirements (Source: VA.gov, https://www.va.gov/resources/getting-emergency-care-at-non-va-facilities/). Miss any of these criteria, and you could be stuck with the entire emergency room bill.

Just like you wouldn’t deploy with only one piece of critical equipment, you shouldn’t navigate retirement healthcare with only one coverage option. You’ve earned VA benefits through your military service AND you’ve paid into Medicare through FICA taxes your entire working life. Why would you rely on just one when you’ve rightfully earned access to both? Smart veterans layer their benefits strategically, creating multiple lines of defense for their healthcare needs.

2. The Four Parts: Decoded for Veterans

Medicare has different parts, and yes, it can seem complicated at first. After nearly two decades in the Medicare industry and helping thousands of veterans navigate these decisions, I can tell you that once you understand how each part works with your existing military benefits, it starts to make sense. Let me break it down in plain English:

Part A: Hospital Insurance

What it covers: Hospital stays, skilled nursing facilities, some home health care, hospice care

2025 cost: $0 for most veterans (you already paid through payroll taxes during your career)

Why veterans need it:

- Keeps TRICARE for Life active for military retirees

- Covers hospital stays anywhere Medicare is accepted

- Required foundation for all other Medicare benefits

Part B: Medical Insurance

What it covers: Doctor visits, outpatient services, preventive care, durable medical equipment, emergency room visits, diagnostic tests, and most medically necessary services outside of hospital stays (Source: CMS.gov, https://www.cms.gov/newsroom/fact-sheets/2025-medicare-parts-b-premiums-and-deductibles)

2025 cost: $185/month standard premium (higher if you have high income due to IRMAA surcharges, which affect about 8% of Medicare beneficiaries) (Source: Veterans Advantage Financial, https://veteransadvantagefinancial.vet/irmaa/)

Why veterans need it:

- Required for TRICARE for Life: we see veterans lose their TRICARE for Life benefits when they don’t maintain Part B enrollment (Source: TRICARE.mil, https://tricare.mil/Plans/Eligibility/MedicareEligible)

- Required for any Medicare Advantage (Part C)

- Backbone of outpatient care nationwide

- Emergency room coverage anywhere in the US, even at facilities that don’t accept Medicare

- Enables access to options that keep Part B premiums as low as possible

Part C: Medicare Advantage

What it covers: Must at least provide every benefit that Part A and B cover, often with additional benefits that VA, Medicare, and TRICARE for Life don’t provide. Medicare states that “Medicare Advantage Plans must cover all of the services that Original Medicare covers” (Source: Medicare.gov, https://www.medicare.gov/basics/get-started-with-medicare/using-medicare/how-to-get-medicare-services)

Average $17/month for Medicare options from private companies, with 75% having no monthly premium. Keep reading to see why they have no monthly premium.

Why veterans need it:

- Allows continued use of VA and TRICARE benefits

- Many options help veterans avoid overpaying for Part B, with nearly one-third (32%) of Medicare options from private companies offering ways to minimize Part B costs in 2025 (Source: KFF.org, https://www.kff.org/medicare/issue-brief/medicare-advantage-2025-spotlight-a-first-look-at-plan-premiums-and-benefits/)

- Additional benefits that VA, Medicare, and TRICARE for Life don’t provide

- Can enhance military benefits, something my team and I specialize in helping veterans achieve

- Emergency room coverage anywhere in the US at any facility. Medicare Advantage plans must cover emergency and urgent care nationwide as in-network services, even if the facility isn’t in the plan’s network. Some Medicare Advantage plans may also include worldwide emergency coverage (Source: AARP, https://www.aarp.org/health/medicare-insurance/info-2024/medicare-coverage-on-vacation.html).

Part D: Prescription Drug Coverage

What it covers: Prescription medications (if not included in Part C)

2025 cost: Average $35-55/month for standalone plans

Why veterans should carefully evaluate Part D:

- VA prescription coverage is “creditable,” meaning there’s no penalty for delaying Medicare Part D as long as you enroll when first eligible or within 63 days of when you no longer have VA health care or other creditable prescription drug coverage (Source: KFF.org, https://www.kff.org/faqs/medicare-open-enrollment-faqs/i-have-drug-coverage-from-the-va-do-i-need-to-sign-up-for-a-part-d-plan/)

- TRICARE for Life includes prescription benefits

- Many Medicare options from private companies include drug coverage at no additional premium

Most veterans already have creditable prescription drug coverage through VA or TRICARE for Life, which protects them from Part D penalties. However, you should evaluate whether Part D might provide better coverage, lower costs, or access to medications not covered by your military benefits. Remember, having multiple prescription options gives you flexibility when the VA formulary doesn’t include a medication you need or when filling prescriptions while traveling.

3. Where the Money Comes From: You’ve Already Paid Your Dues

Something that might surprise you: Remember those old pay stubs from your military service and civilian career? There was a line item called “FICA”, the Federal Insurance Contributions Act tax that funds Social Security and Medicare. During my extensive time in the industry, I’ve seen thousands of veterans who don’t realize they’ve already paid for these benefits.

Think about it this way: if you earned around $50,000 a year over a 40-year career, you and your employers contributed about $58,000 toward Medicare through those FICA taxes on your pay stub at the current rate of 2.9% (Source: IRS.gov, https://www.irs.gov/taxtopics/tc751). If you averaged more than $50,000 per year, then a higher amount has been paid into Medicare by you and your employers. So when we talk about Medicare benefits, you’re not getting something “free.” You’re collecting on an investment you’ve been making your entire working life.

Many veterans we work with make a costly mistake. They skip Medicare Part B with the thought, “I have VA benefits, and that’s enough.” What they’re really saying is they don’t want to pay the Part B premium, and I don’t blame them for that concern.

This changes how you should think about Medicare costs: there are now Medicare options from private companies with premiums as low as $0 that help keep your Part B costs as low as possible.

Not enrolling in Part B is like walking away from decades of your own contributions to Medicare. You’ve already paid into the system your entire working life. Why would you walk away from benefits you’ve already paid for?

The bigger picture changes how you should think about Medicare costs. Those Medicare options from private companies with premiums as low as $0 aren’t really free. They’re funded partly by the taxes you already paid over decades of work. And when an option helps you avoid overpaying for Part B, you’re keeping more of what’s rightfully yours based on decades of FICA contributions.

My dad, Wallace Duncan, an 82-year-old Vietnam-era veteran, understands this perfectly. Through his Medicare option from a private company, he obtains the lowest possible Part B premium while maximizing additional benefits. This isn’t charity from an insurance company. It’s making the most of the investment he’s made through decades of payroll taxes. We help veterans access similar strategies to avoid overpaying for their Part B coverage.

4. Three Critical Reasons Veterans Cannot Ignore Medicare

Throughout my Medicare career, I’ve discovered unique challenges veterans face that most advisors never understand. I’ve seen what happens when veterans ignore Medicare thinking their military benefits are enough. Let me share the three most critical reasons my team and I tell every veteran they absolutely cannot afford to ignore Medicare.

Reason #1: VA Funding and Eligibility Can Change

The VA budget is set by Congress every year, and recent events prove how unpredictable this can be. In 2024, VA faced a $6.6 billion budget shortfall that required emergency congressional action to prevent service cuts (Source: Federal News Network, https://federalnewsnetwork.com/budget/2024/11/va-updates-fy-2025-health-care-budget-shortfall-to-6-6b-nearly-half-its-previous-estimate/).

We have worked with veterans who suddenly faced reduced VA services due to budget constraints they had no control over. Funding levels, eligibility criteria, and covered services can shift based on political decisions that have nothing to do with your needs. Your VA care might be affected by factors completely outside your control.

Medicare, however, is a federal entitlement. I hate the word entitlement because it implies something given rather than earned, when you’ve actually paid into Medicare your entire working life through FICA taxes. You’ve earned and paid for these benefits your entire working life. Once you’re enrolled, your coverage is guaranteed by law. It’s security you control, not politicians.

Reason #2: Emergency Freedom Nationwide

In a medical emergency, any hospital must treat you, even if it’s not a VA facility. But the catch is that the VA might not cover the bills if they determine it wasn’t an approved emergency or if you could have reasonably reached a VA facility.

Original Medicare and Medicare Advantage (Part C) provide universal emergency coverage at any hospital in the United States. I’ve worked with veterans who were vacationing in Florida when they had to go to the emergency room, 200 miles from the nearest VA facility. Their Medicare coverage meant immediate treatment without worrying about VA approval or massive bills. That’s the kind of protection every veteran needs, especially if you travel or live far from VA care.

Reason #3: TRICARE for Life Depends on It

If you’re a military retiree with TRICARE for Life, listen carefully: TRICARE for Life requires you to have both Medicare Part A and Part B. Skip Part B, and you lose TRICARE for Life entirely. This isn’t optional. Federal law (10 U.S.C. § 1075) specifically requires both Medicare Parts A and B to maintain TRICARE for Life eligibility (Source: TRICARE.mil, https://tricare.mil/Plans/Eligibility/MedicareEligible).

I’ve worked with military retirees who lost their TRICARE for Life benefits because they tried to skip Part B to save money. Once you lose TFL, getting it back requires enrolling in Medicare and potentially facing late enrollment penalties for the rest of your life.

Enrolling in Medicare on time ensures you keep this valuable benefit that acts as outstanding secondary coverage, eliminating virtually all out-of-pocket costs for covered medical services. When we work with career military veterans who have TRICARE for Life, we call it the ‘golden ticket’ of medical coverage. But that golden ticket only works if you maintain at least Medicare Parts A and B. Skip either one, and you lose this incredible benefit that you’ve earned through 20+ years of service.

Understanding these critical reasons is important, but it’s equally important to understand why generic Medicare advice consistently fails veterans.

5. Where Generic Medicare Advice Falls Short for Veterans

My team and I have cleaned up countless messes created by generic Medicare advisors who treat every 65-year-old the same way. The standard advice they give veterans is the exact same advice they give everyone else:

- “Just get a Medicare Supplement plan to cover the gaps”

- “Medicare Advantage plans limit your doctor choices”

- “You should always enroll in Part D to avoid penalties”

- “Original Medicare is always better than Medicare Advantage”

For civilian retirees, this one-size-fits-all approach might work. But veterans aren’t civilian retirees. Veterans have earned unique benefits through their service, and these benefits fundamentally change what makes sense for Medicare coverage.

The Veterans-Specific Questions Generic Advisors Never Ask

When we work with veterans, we start with questions that generic advisors never think to ask:

- Do you have TRICARE for Life?

- What’s your VA priority group?

- Do you use VA Community Care?

- How far do you live from VA facilities?

- What percentage of your care comes from the VA versus civilian providers?

These critical factors determine your optimal Medicare strategy. Generic advisors who don’t understand military benefits consistently provide advice that costs veterans thousands while missing valuable opportunities they’ve earned through their service.

Real-World Example: The Cookie-Cutter Failure

A career Air Force veteran contacted us after working with a generic Medicare advisor who recommended Original Medicare plus a $189 monthly Medigap Plan G because “it’s the gold standard.” The advisor never asked about military benefits or considered veteran-specific alternatives.

The generic advisor missed several critical points:

- The veteran had TRICARE for Life, making Medigap completely unnecessary

- A Medicare option from a private company in his area helped keep his Part B premium as low as possible

- The same option included additional benefits that VA, Medicare, and TFL don’t provide

- He could have been paying far less monthly while gaining additional benefits

The cost of generic advice: $3,948 annually in missed opportunities.

The Independence Advantage

We are completely independent. We don’t work for any insurance company or receive bonuses for recommending specific plans. When generic advisors tied to specific companies tell you “this is the best plan available,” they’re really saying “this is the best plan my company offers.”

We can evaluate every plan available in your area to find the one that actually maximizes your veteran benefits. This independence means we can recommend any solution that’s right for you, whether that’s Original Medicare, Medigap, or Medicare Advantage, without being restricted to specific companies or plan types.

What Makes Veteran-Specific Expertise Different

As specialists who work exclusively with veterans, we understand how Medicare works alongside your existing military benefits to create comprehensive coverage. We analyze how Medicare works alongside VA priority groups, TRICARE for Life requirements, and service-connected disability considerations.

Our expertise means recognizing that veterans with TRICARE for Life already have coverage that functions better than any Medicare Supplement plan, eliminating virtually all out-of-pocket costs. We understand that veterans often prefer specific provider networks through established VA relationships or TRICARE providers, making Medicare Advantage PPO plans particularly valuable for maintaining continuity of care while adding flexibility.

We evaluate prescription drug options knowing that TRICARE for Life includes robust pharmacy benefits through Express Scripts, while also understanding when Medicare Part D might provide access to medications not on the VA formulary or offer more convenient pharmacy options during travel. This complete understanding allows us to develop strategies that maximize every benefit you’ve earned through military service.

Now that you understand the basics, let me share the costly mistakes I see veterans make when they get generic Medicare advice instead of veteran-specific guidance.

6. Common Mistakes Veterans Make (And How Specialists Help You Avoid Them)

Working exclusively with veterans has shown me the same costly mistakes happen over and over when veterans rely on generic Medicare advice. Here are the four biggest missteps that cost veterans thousands:

Mistake #1: Waiting Past 65 to Enroll in Part B

Many veterans think, ‘The VA covers me, I’ll sign up later.’ This is one of the most expensive mistakes you can make. For every 12-month period you delay Part B after your Initial Enrollment Period, you face a lifelong 10% penalty on your Part B premium.

Wait just two years and you’ll pay an extra $37 monthly ($444 annually) based on today’s premium, but the kicker is that as Part B premiums increase every year, your penalty grows too because it’s a percentage of the current premium, not a fixed dollar amount. Over 20 years, that 20% penalty could easily cost you $10,000 or more (Source: Medicare.gov, https://www.medicare.gov/basics/costs/medicare-costs/avoid-penalties).

On a regular basis we have veterans that call us at age 70, 75 wanting to put their Part B in place, because the VA health system isn’t meeting all their needs. As my dad Wallace says, “Chris, the VA health system is great, but it ain’t perfect.” When veterans realize the VA can’t meet all their needs and try to add Part B, they discover they face both waiting periods and lifetime penalties.

They contact Social Security to try and put their Part B in place only to learn they have to wait for the general enrollment period that goes from January 1 to March 31, but the big shock is the Part B premium penalty they have to pay every month for the rest of their life.

On a regular basis, veterans tell us about the conflicting advice they received before calling us. A VA representative assured them their VA coverage would protect against Part B penalties. Their doctor at the VA told them they didn’t need Part B. In some cases, even a Social Security representative suggested they skip Medicare to save money since they have VA coverage.

While these professionals mean well, they often aren’t aware that Medicare options from private companies can help veterans keep their Part B premiums as low as possible, making coverage more affordable than they realize.

Veteran Medicare specialist insight: VA coverage is not creditable coverage for Medicare Part B penalty purposes. According to Medicare.gov, only employer group health plan coverage allows you to delay Part B enrollment without penalties, and VA coverage does not qualify (Source: Medicare.gov, https://www.medicare.gov/basics/get-started-with-medicare/medicare-basics/working-past-65).

Mistake #2: Thinking TRICARE for Life Replaces Medicare

TRICARE for Life doesn’t replace Medicare. It works alongside Medicare as wraparound coverage, also called secondary coverage. Without at least Medicare Parts A and B, TRICARE for Life simply doesn’t function. TRICARE for Life also provides wraparound coverage for Medicare Part C (Medicare Advantage).

Veteran Medicare specialist insight: Medicare (Parts A, B, or C) pays first, TFL covers what’s left, giving you virtually zero out-of-pocket costs.

Mistake #3: Dismissing Medicare Advantage (Part C) Plans

Some veterans think Medicare Advantage is only for civilians or that it will interfere with their VA benefits. This misconception costs them thousands in missed benefits.

Veteran Medicare specialist insight: Many Medicare options from private companies work well for those with VA benefits and/or TRICARE for Life. They don’t interfere with your military benefits. They enhance them with additional benefits that VA, Medicare, and TFL don’t provide while helping you avoid overpaying for Part B.

Mistake #4: Believing TRICARE for Life Won’t Work with Medicare Advantage (Part C)

This might be the most damaging misconception of all. Many veterans are told by TRICARE representatives, VA staff, or even generic Medicare advisors that “TRICARE for Life doesn’t work with Medicare Advantage plans” or that “you’ll lose your TRICARE benefits if you choose Part C.” This is completely false and costs veterans thousands in missed benefits.

According to the official TRICARE website, “If you enroll in a Medicare Advantage Plan, you still have Medicare. Medicare is still your primary coverage, and TRICARE For Life is the second payer for TRICARE-covered services” (Source: TRICARE.mil, https://tricare.mil/FAQs/TRICARE-with-Medicare/TRIMed_Advantage).

The only difference is that Medicare Advantage claims don’t automatically crossover to TRICARE, so you may need to file claims manually for TRICARE-covered services.

Real-world veteran Medicare specialists have an advantage over generalists. Specialists understand how the system actually works in practice, not just what’s written in a manual. Medical providers run businesses, and as they serve more Medicare-eligible patients, they’ve learned how to streamline billing for maximum reimbursement.

Most providers who work with TRICARE beneficiaries already know how to bill TRICARE for Life directly through Wisconsin Physician Services (WPS), which administers TFL. We haven’t had a client need manual claim forms in over two years because providers have streamlined their processes for Medicare beneficiaries and understand how to bill WPS for the TFL portion of the bill.

Veteran Medicare specialist insight: Many Medicare options from private companies offer significant benefits that veterans miss out on because of this misconception. These include ways to minimize Part B premiums and add additional benefits that VA, Medicare, and TRICARE for Life don’t provide. TRICARE for Life provides wraparound coverage for both Original Medicare and Medicare Advantage plans from private companies that contract with Medicare, allowing veterans to access these additional benefits while maintaining comprehensive coverage.

7. The Power of Veteran-Focused Guidance

When my team and I work with veterans, we don’t start with generic Medicare questions. We start with questions like:

- Do you have TRICARE Prime or Select? (if under 65)

- Do you have a spouse or children on your TRICARE Prime or Select?

- Do you have TRICARE for Life?

- What’s your VA priority group?

- Do you use Community Care?

- Do you have any level of disability?

- How far do you live from VA facilities?

- Do you get your prescription from a VA facility?

- If so, do you get them directly at a VA facility or through mail order?

- What percentage of your care do you get through the VA versus civilian providers?

- Do you travel frequently or spend time in multiple states?

These aren’t questions that generic Medicare advisors even know to ask, but they’re absolutely crucial for developing the right strategy for your situation. For example, a veteran who’s 100% service-connected and lives next to a VA medical center needs a completely different Medicare strategy than a veteran with 20% disability who uses VA care occasionally and travels frequently between states.

What really frustrates me is that I regularly see veterans who were told by generic advisors that “VA coverage means you don’t need Medicare” or “just get Original Medicare with a Supplement plan like everyone else.”

These advisors don’t understand that VA coverage provides no protection from Medicare Part B penalties, or that military retirees with TRICARE for Life are wasting thousands annually on unnecessary Medigap policies. They treat veterans like any other Medicare enrollee instead of recognizing the unique integration opportunities and financial benefits that military service has earned.

Veterans who work with specialists consistently end up with better outcomes including lower out-of-pocket costs, more comprehensive coverage, and Medicare strategies that enhance their military benefits instead of competing with them.

This is exactly what We Speak Veteran™ means in practice. We don’t just understand Medicare. We understand how your specific military situation changes everything about what makes sense for your Medicare strategy. We speak your language because we specialize exclusively in veterans, not because we slapped a military logo on generic Medicare advice.

8. Key Takeaways for Veterans

Let me recap the essential points every veteran needs to understand:

✓ Medicare is your nationwide safety net that works alongside (not instead of) your VA benefits and keeps TRICARE for Life active

✓ Part A is usually premium-free, Part B costs $185/month in 2025 and missing Part B enrollment can lead to costly lifetime penalties, according to the Centers for Medicare & Medicaid Services (Source: CMS.gov, https://www.cms.gov/newsroom/fact-sheets/2025-medicare-parts-b-premiums-and-deductibles)

✓ Medicare Advantage (Part C) doesn’t cancel your VA or TRICARE benefits. It can enhance them while minimizing your Part B premiums

✓ You’ve already earned these benefits through decades of FICA taxes from military service and civilian work: you’re not asking for handouts, you’re collecting on an investment you’ve already made

✓ Generic Medicare advice consistently fails veterans: you need guidance from specialists who understand how military benefits change everything about your Medicare strategy

✓ The right strategy integrates all your benefits to create coverage that’s often better and less expensive than what civilian retirees can access

✓ TRICARE for Life and Medicare Advantage (Part C) work together effectively: Medicare Advantage pays first, then TRICARE for Life covers most or all of your remaining costs, often leaving you with zero out-of-pocket expenses

These aren’t just facts to memorize. They’re the foundation of a Medicare strategy that protects everything you’ve earned through your service.

9. What’s Coming Next

Now that you understand Medicare basics from a veteran’s perspective, Chapter 2 will dive into a crucial question: How exactly do VA health benefits and Medicare complement each other? Can they coexist without creating conflicts?

The answer is yes, and when integrated properly by someone who understands both systems, they create a powerful combination that gives you the best of both worlds.

I’ll show you how smart veterans use both systems strategically, the specific situations where Medicare fills critical gaps in VA coverage, including emergency care away from the VA and access to specialists when the VA can’t provide them quickly enough.

Most importantly, I’ll help you avoid the costly mistakes that generic Medicare advisors regularly make with veterans: mistakes that can cost you money every single month for the rest of your life.

Questions about how Medicare works with your specific VA or TRICARE benefits? My team and I help veterans navigate these decisions every day. Call us at 888-960-8387 (VETS) for personalized guidance that demonstrates what WE SPEAK VETERAN™ really means.

Chapter 3: TRICARE for Life and Medicare

How military retirees keep world-class coverage, and why Parts A & B are absolutely mandatory

1. Do You Qualify for TRICARE for Life?

Let’s start by making sure we’re talking about you. TRICARE for Life (TFL) is arguably one of the best healthcare benefits available to any group of Americans, but not every veteran qualifies. Understanding the requirements is crucial because the rules are non-negotiable.

You’re eligible for TFL if:

- You served 20+ years of active duty (or equivalent Guard/Reserve time)

- You’re enrolled in both Medicare Parts A and B

- You’re a qualified spouse or dependent of an eligible military retiree

The part that trips up many military retirees is this: You must have Medicare Parts A and B. Not just Part A. Not “eventually” Part B. Both parts, active and current. Period.

Some medical retirees with disability ratings also qualify, but the Medicare requirement remains exactly the same for everyone. No exceptions, no special circumstances, no waivers.

Many attempt to skip Part B to save on the monthly premium, but this can be a costly mistake. What they often don’t realize is that doing so also leaves them exposed to lifelong penalties on their Part B premium if they enroll later.

Furthermore, there are many Medicare options with premiums as low as $0 that can help you avoid overpaying for Part B. These options also work with TFL, with TFL providing wraparound coverage for any deductibles, copays, and coinsurance the option doesn’t cover. Choosing to skip Part B means missing out on these valuable benefits you’ve earned.

2. Why Medicare Parts A & B Are Absolutely Non-Negotiable

This isn’t a suggestion from some bureaucrat; it’s federal law written into the statute that created TRICARE for Life. Let me explain why this requirement exists and why you absolutely cannot get around it.

It’s Written in Federal Law

TRICARE for Life was established by Public Law 106-398 (Fiscal Year 2001 National Defense Authorization Act) and is currently governed by 32 CFR § 199.17, which specifically requires both Medicare Parts A and B. The regulation is crystal clear: “when a retiree or retiree family member becomes individually eligible for Medicare Part A and enrolls in Medicare Part B, he/she is automatically eligible for TRICARE-for-Life.” (Source: Law.Cornell.edu, https://www.law.cornell.edu/cfr/text/32/199.17)

The law specifically states that TFL can only function as secondary coverage after Medicare pays first. This means that whether you have Original Medicare or a Medicare Advantage (Part C) plan, your Medicare coverage acts as the primary payer before TFL.

Think of it this way. Medicare is the engine, and TFL is the transmission. You need both for the system to work.

The Financial Architecture

TFL was designed as a “wraparound” benefit that eliminates most out-of-pocket costs after your primary Medicare coverage pays its portion. This means that whether you have Original Medicare or a Medicare Advantage (Part C) plan, the entire financial structure depends on your Medicare coverage being the primary payer:

- Your Medicare coverage pays the majority of your medical bills first

- TRICARE for Life covers what Medicare doesn’t pay

- You end up with virtually zero out-of-pocket costs

Without this Medicare foundation, TFL has nothing to “wrap around” and simply cannot function.

Preventing System Gaming

The Medicare requirement also prevents people from only enrolling when they get sick. If military retirees could choose whether to have Medicare, many healthy retirees might skip it and only enroll when they developed serious health problems. This would drive up costs for everyone and destabilize both systems.

3. How Your Medicare Coverage and TFL Work as a Perfect Team

When you have both your Medicare coverage (whether Original Medicare or a Medicare Advantage plan) and TRICARE for Life active, this is exactly what happens when you receive medical care.

Step 1: Your Medicare Coverage Pays First

Your healthcare provider submits the claim to your Medicare coverage first. Your Medicare plan processes it according to its rules and pays its portion based on Medicare’s approved amount.

Step 2: TRICARE for Life Processes the Remaining Balance

The way TRICARE for Life receives the claim depends on your Medicare choice.

If You Have Original Medicare: Medicare electronically forwards the claim information to Wisconsin Physician Services (WPS), which administers TRICARE for Life. You typically don’t need to file a separate claim or do anything, as this integration happens automatically to cover your deductibles, copays, and coinsurance.

If You Have a Medicare Advantage (Part C) Plan: Your provider will send the claim to your Part C plan, which pays the majority of the cost. Then, it’s common for your provider to send the remaining deductible, copay, or coinsurance portion directly to Wisconsin Physician Services (WPS), which administers TRICARE for Life. WPS then pays the medical provider the amount owed.

We’ve learned that most providers already know how to bill properly, often because they accept TRICARE Prime or Select. If a provider does not bill TFL directly, DD Form 2642 is available for you to submit to get reimbursed for any deductible, copay, or coinsurance payments you make to your provider (Source: Department of Defense, https://www.esd.whs.mil/Portals/54/Documents/DD/forms/dd/dd2642.pdf). While we used to provide this form to clients frequently in the past, we have not been asked for it in several years. This is because medical provider offices are becoming increasingly accustomed to billing different entities as more of their patients age into Medicare.

Step 3: You End Up with Near-Zero Out-of-Pocket Costs

TRICARE for Life reviews what your Medicare coverage paid and automatically covers most of what Medicare didn’t pay, including deductibles, coinsurance, and copays.

4. Real Example: How It Works

If you have Original Medicare

Let’s say you need outpatient surgery that costs $8,000:

- Medicare Part B deductible: You pay $257 (2025 amount)

- Medicare pays 80%: $6,194 of the remaining balance

- Medicare coinsurance (20%): $1,549 you would normally owe

- TFL pays the deductible and coinsurance: $1,806

- Your total out-of-pocket cost: $0

If you choose Medicare Part C with the same $8,000 outpatient surgery

Most Part C plans have flat copays for outpatient surgery, and many also have a $0 deductible. For this example, we will say the copay is $1,000; if there is a deductible, TFL will pay that as well.

- TFL pays $1,000 copay

- Your total out-of-pocket cost: $0

This integration creates virtually bulletproof coverage. I’ve seen military retirees go through major medical events (cancer treatments, heart surgeries, extended hospital stays) and walk away with minimal or zero bills.

5. The Generic Advisor Mistake: Selling Unnecessary Medigap

Here’s where I see the most expensive mistake that military retirees make, often because they get advice from generic Medicare advisors who don’t understand TRICARE for Life.

A typical Medicare advisor sees a military retiree approaching 65 and thinks, “This person needs Medicare Supplement insurance to cover the gaps.” So they recommend a Medigap Plan G for $125-$300 per month.

The problem: TRICARE for Life already functions as the best Medicare Supplement insurance available. In fact, it works better than Medicare Supplement from private insurance companies because it will pay deductibles, copays and coinsurance for Medicare Part C plans. A Medicare Supplement policy will not do that. This unique feature of TFL means military retirees get comprehensive coverage with both Original Medicare and Medicare Advantage plans. Buying a separate Medigap policy when you have TFL is like buying a second car when you already have perfect transportation.

We’ve helped military retirees who were paying $3,000+ annually for Medigap policies they absolutely didn’t need. That’s $30,000 over 10 years for duplicate coverage.

The specialist difference: When we work with military retirees, the first question we ask is about their TRICARE for Life status. Generic advisors often don’t even know what TFL is, let alone how it integrates with Medicare.

6. Medicare Advantage (Part C) with TRICARE for Life: A Powerful Combination

This is where many military retirees can significantly enhance their benefits while keeping their Part B premiums as low as possible.

When you enroll in a Medicare Advantage (Part C) plan, it is your primary insurance, but TRICARE for Life continues to work exactly the same way as your secondary coverage or wraparound coverage, paying deductibles, copays and coinsurance. It’s important to know that when you have Part C you still have Medicare. As TRICARE’s official website confirms: “If you enroll in a Medicare Advantage Plan, you still have Medicare. Medicare is still your primary coverage, and TRICARE For Life is the second payer for TRICARE-covered services.” (Source: TRICARE.mil, https://tricare.mil/FAQs/TRICARE-with-Medicare/TRIMed_Advantage)

Why This Combination Works So Well

Minimizing Part B Premiums: Some Medicare options with premiums as low as $0 help keep your Part B costs as low as possible. With TFL covering your deductibles, copays and coinsurance, minimizing what you pay for Part B provides maximum value.

Additional Benefits Part C Provides that TFL Doesn’t Cover:

- Medicare options with premiums as low as $0 can provide access to additional benefits that enhance your overall healthcare coverage beyond what VA, Medicare, and TFL offer.

(Source: 2026 Medicare and You Handbook Page 62, Medicare.gov, https://www.medicare.gov/publications/10050-medicare-and-you.pdf)

Real Example:

A husband and wife both have TRICARE for Life. They enrolled in Medicare options with premiums as low as $0 that help them avoid overpaying for Part B.

The result:

- Combined Part B premium savings throughout retirement

- Additional healthcare benefits not available through TFL alone

- Enhanced coverage value

All while keeping their full TRICARE for Life benefits unchanged.

TRICARE for Life Prescription Coverage

TFL includes comprehensive prescription drug coverage, which operates differently from Medicare Part D:

Where You Can Fill Prescriptions:

- Military pharmacies (often $0 cost)

- VA pharmacies (if you’re also enrolled in VA care)

- Express Scripts home delivery

- Network retail pharmacies nationwide

Important Note About Medicare Part D: Since TFL provides creditable prescription drug coverage, you can delay Medicare Part D enrollment without penalty. If you choose a Medicare Advantage (Part C) plan with drug coverage, you can evaluate whether that option or Express Scripts provides better value for your specific medications. Many Medicare Advantage plans include Part D prescription coverage at $0 additional monthly premium, giving you another option to consider alongside your TFL prescription benefits.

7. Where Generic Advisors (and Even TFL Guidance) Get TRICARE for Life Wrong

We regularly clean up messes created by well-meaning generalist Medicare advisors who don’t understand military benefits. Here are the most common errors, and a crucial distinction regarding TRICARE for Life’s own advice:

Mistake #1: Recommending Medigap with TFL

- What they say: “You need Plan G to cover Medicare’s gaps.”

- The reality: TFL already covers those gaps better than any Medigap plan.

- The cost: $2,000-$4,000 annually in wasted premiums.

Mistake #2: Avoiding Medicare Advantage (Part C)

- What they say: “Advantage plans will interfere with your military benefits.”

- The reality: Medicare Advantage (Part C) plans also work with TFL and often provide additional benefits.

- The cost: Overpaying for Part B and missing access to additional benefits.

Mistake #3: Ignoring TFL Integration (The TFL Guidance Gap)

- What they say: “Let’s just set you up like any other Medicare client” or “You only need Medicare Parts A & B for TRICARE for Life.”

- The reality: While it’s true that you only need A & B to maintain TFL, this advice, even from well-meaning TRICARE representatives, often stops short of presenting the full spectrum of Medicare options available to military retirees. TFL staff are experts on TRICARE, not necessarily on the intricacies of Medicare and Medicare Part C plans and how they can enhance TFL benefits. Military retirees need strategies that account for TFL’s unique benefits and the potential added value of a Part C plan.

- The cost: Suboptimal coverage, missing strategies to avoid overpaying for Part B, and no access to additional benefits that Medicare options can provide without interfering with your TFL.

When we work with military retirees, we don’t just recommend Medicare plans. We develop strategies that optimize the integration between Medicare, TRICARE for Life, and any other benefits they might have.

Common Questions with Straight Answers

Q: “If Medicare pays first, why do I still need TFL?”

A: Because TFL eliminates your deductibles, coinsurance, and copays, giving you near-zero out-of-pocket costs. Without TFL, you’d be responsible for all of Medicare’s cost-sharing requirements.

Q: “Can I drop Medicare Part B if I move overseas?”

A: Absolutely not. Even if you live overseas where Medicare doesn’t provide coverage, you must maintain Part B to keep your TFL eligibility. This is a common misconception that costs military retirees their TFL benefits. TFL can also provide coverage overseas. (Source: TRICARE.mil, https://tricare.mil/Plans/HealthPlans/TFL/TFL_O)

Q: “Will a Medicare Advantage (Part C) plan interfere with my military healthcare on base?”

A: Not at all. You can continue using base clinics, hospitals, and pharmacies exactly as before. The Medicare Advantage (Part C) plan simply gives you additional civilian options.

Q: “What if I don’t like my Medicare Advantage (Part C) plan?”

A: According to TRICARE’s official newsroom, “Because you have TFL, you may disenroll from a Medicare Advantage Plan at any time. You can call Medicare or your Medicare Advantage Plan to request disenrollment. You’ll automatically be back in Original Medicare.”

Source: TRICARE Newsroom

8. Key Takeaways for Military Retirees

✓ Medicare Parts A & B are mandatory to maintain TRICARE for Life—never let them lapse

✓ Medicare + TFL creates unbeatable coverage with virtually no out-of-pocket costs

✓ Medicare Advantage (Part C) can enhance your benefits while keeping Part B premiums as low as possible

✓ Never buy Medigap if you have TFL—you’re paying for duplicate coverage

✓ Independent veteran specialists understand the integration better than generic Medicare advisors

✓ Annual reviews ensure you’re maximizing both benefits as plans and options change

✓ The right strategy keeps your Part B premiums as low as possible while maintaining world-class healthcare coverage

9. What’s Coming Next

Now that you understand how TRICARE for Life works with Medicare, you may have questions about Medicare Advantage plans. There’s a lot of criticism out there. Articles, studies, and “consumer advocates” claim these plans restrict care, deny services, and shortchange beneficiaries.

But after nearly two decades in Medicare and now working exclusively with veterans, I’ve discovered much of this criticism is outdated, misleading, or comes from sources with financial interests in keeping people in Original Medicare.

Chapter 4 will show you what the data actually reveals about Medicare Advantage.

We’ll examine the actual 2024 and 2025 data on approval rates, quality measures, and beneficiary satisfaction. You’ll see why 54% of Medicare beneficiaries have chosen Medicare Advantage, and why thousands of clients choose these plans to enhance their TRICARE for Life coverage while keeping Part B premiums as low as possible.

You’ll discover who’s really behind the anti-Medicare Advantage campaign and why their financial interests may not align with yours as a veteran. By the end of Chapter 4, you’ll have the facts you need to evaluate Medicare Advantage objectively.

Ready to separate fact from fiction? Let’s examine what the data reveals.

Questions about how TRICARE for Life integrates with your Medicare options? Throughout my Medicare career spanning nearly two decades, now working exclusively with veterans, I’ve helped thousands of military retirees navigate these integration decisions. Call us at 888-960-8387 (VETS) for expert guidance that shows you exactly what WE SPEAK VETERAN™ really means.

Chapter 5 — How Veterans Can Avoid Overpaying for Medicare Part B

Putting real money back in your Social Security check every single month

1. How Veterans Access the Lowest Possible Part B Premium

Throughout your military career, you learned to maximize every benefit available to you. You understood your housing allowance, your combat pay, your retirement benefits. Now there’s another opportunity you’ve earned that most veterans never hear about: ensuring you’re not overpaying for Medicare Part B.

My dad, Wallace Duncan, is an 82-year-old Vietnam-era veteran who obtains the lowest possible Part B premium through his Medicare option from a private company. While the standard Part B premium in 2026 is $206.50 monthly, his chosen Medicare option ensures he’s getting maximum Medicare benefits for minimum premium cost. This isn’t a temporary promotion or a special deal. It’s how certain Medicare options work, and he maintains excellent healthcare coverage.

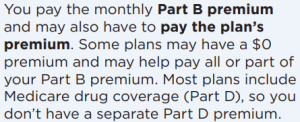

Wallace isn’t unique. My team and I have helped thousands of veterans ensure they’re not overpaying for their Medicare Part B premium. The 2026 Medicare & You handbook states on page 11 that “Some plans may help pay all or part of your Part B premium.” Yet most veterans still don’t know these opportunities exist.

Page 11 2026 Medicare and You Handbook: https://www.medicare.gov/publications/10050-medicare-and-you.pdf

Medicare options from private companies that contract with Medicare have premiums as low as $0 per month. The Medicare & You handbook confirms that some of these options can help pay all or part of your Part B premium. Remember, you’ve contributed to Medicare through FICA your whole working life. If you earned around $50,000 a year over a 40-year career, you and your employers contributed about $58,000 toward Medicare through those FICA taxes on your pay stub at the current rate of 2.9%. (Source: IRS.gov, https://www.irs.gov/taxtopics/tc751)

When you find Medicare options that work this way, you’re ensuring you’re not overpaying for coverage you’ve already earned through decades of contributions. You’re getting maximum Medicare benefits while paying the minimum premium possible.

How This Works:

If Social Security deducts your Part B premium, you’ll see the impact in what’s taken from your Social Security benefit each month, leaving more in your Social Security benefit every month. If you pay Medicare directly, you’ll see the amount on your quarterly Medicare bill.

The key insight: You’ve already paid into Medicare your entire working life. Finding the right Medicare option ensures you’re not leaving money on the table and that you’re obtaining the lowest Part B premium available in your area.

2. Why Veterans Are Well-Positioned for the Lowest Part B Premiums

Veterans consistently obtain the lowest Part B premiums available, and there’s a mathematical reason for this. Insurance companies recognize that veterans with VA coverage or TRICARE for Life represent what they call “favorable selection.”

Reduced Claims Risk

When you have VA coverage or TRICARE for Life in addition to your Medicare, you represent a different risk profile to insurance companies. Veterans typically use their Medicare coverage strategically for emergency situations when away from VA facilities, specialist care not available through the VA, convenience when traveling, and second opinions from civilian doctors.

With TRICARE for Life, Medicare (whether Original or from a private company that contracts with Medicare) pays first, then TFL provides wraparound coverage for the remaining deductibles, copays, and coinsurance. This dual coverage creates stability that insurance companies recognize and value, since they know TFL’s wraparound coverage will handle costs Medicare doesn’t cover. Your military service and the benefits you’ve earned actually help you obtain lower premiums.

Stable Healthcare Patterns

Veterans bring unique advantages to the Medicare marketplace. You’ve spent years navigating military healthcare systems. You understand how to work within structured healthcare environments. You typically have established relationships with VA providers for routine care and make informed decisions about when to use different benefit systems.

This stability and healthcare literacy make veterans attractive to insurance companies. They know you’ll use benefits appropriately and maintain consistent care patterns.

Geographic Stability

Many veterans establish roots in communities near military installations or VA facilities. This geographic stability provides insurance companies with members less likely to move out of their service areas frequently. When insurance companies can count on stable membership, they’re willing to help veterans access the lowest possible Part B premiums.

We specifically look for insurers who understand these veteran patterns and value them accordingly. The result is that veterans consistently obtain lower Part B premiums compared to the general Medicare population.

3. The Current Market Reality for 2025

dramatically. Research from the Kaiser Family Foundation shows significant growth in these opportunities. According to KFF analysis of CMS data, approximately 32% of Medicare options from private companies that contract with Medicare now offer a reduction in the Part B premium, up from just 19% the previous year. (Source: KFF.org, https://www.kff.org/medicare/issue-brief/medicare-advantage-2025-spotlight-a-first-look-at-plan-premiums-and-benefits/)

Understanding What’s Available:

Among the options offering a reduction in the Part B premium, KFF data shows:

- 28% offer $100 or more monthly in Part B premium reduction

- 25% offer $50.01-$100 monthly in Part B premium reduction

- 17% offer $10.01-$50 monthly in Part B premium reduction

- 30% offer $0.01-$10 monthly in Part B premium reduction

Veterans are well-positioned to access options that help ensure they’re not overpaying for Part B. My team and I have helped thousands of veterans obtain the lowest Part B premiums available in their areas.

Geographic Variations That Matter

Your location significantly impacts what options are available to help you avoid overpaying for Part B. Several factors influence this:

- Local healthcare costs in your area

- Competition among insurance companies

- Medicare payment rates set by CMS

- Concentration of VA facilities

High-opportunity areas (often counties with strong VA presence): Veterans can find options where they’re paying far less for Part B than the standard premium

Moderate-opportunity areas (suburban locations): Veterans have good options for obtaining lower Part B premiums

Limited-opportunity areas (urban centers with high medical costs): Veterans may find fewer options to significantly lower their Part B costs

Understanding these variations is critical. A typical advisor might not know what’s available in your specific area, showing you an option where you’re still overpaying when better options exist just by choosing a different insurer. The difference between advisors who specialize in your area versus those who don’t can mean paying substantially more or less for the same Medicare coverage.

4. The Financial Impact Over Your Retirement

Numbers on a page are one thing. Real money staying in your pocket is another. Let me show you why understanding what’s available in your area matters for your long-term financial security.

The difference between paying the standard Part B premium versus obtaining the lowest premium available in your area compounds significantly over time. Over a typical 20-year retirement, this difference can represent substantial savings—enough money to fund major life goals like helping grandchildren with education, enjoying travel and experiences, providing financial security and peace of mind, or maintaining a higher quality of life throughout retirement.

If Social Security deducts your Part B premium, obtaining a lower premium means more staying in your Social Security benefit each month. If you pay Medicare directly, it means lower quarterly Medicare bills. Either way, the financial impact accumulates year after year.

The opportunities to obtain lower Part B premiums can change from year to year as insurance companies adjust their offerings. We conduct annual reviews with our clients to ensure you’re always in the option with the best benefits for your specific needs. We’ve actually seen opportunities to help with Part B premiums increase over the years as insurance companies compete harder for veteran clients.

This is why working with specialists who understand what’s available in your specific area matters. The difference between an advisor who shows you one option versus a specialist who evaluates all available options can significantly impact your retirement finances.

5. How to Access Options That Help Ensure You’re Not Overpaying for Part B

Understanding how to access the best Part B cost strategies requires knowing where to look and what questions to ask. Generic Medicare advisors often miss these opportunities because they don’t specialize in veteran situations.

Step 1: Identify Available Options

Start with Medicare.gov’s Plan Finder, but don’t stop there. Filter specifically for Medicare options from private companies listing “Part B premium reduction” in their benefits summary. Look beyond the first few results. Some of the best opportunities for veterans come from regional insurers that understand military communities.

We have developed proprietary tools that allow identification of the options that can help minimize your Part B costs in minutes, compared to the hours it might take using Medicare.gov alone.

Step 2: Verify What’s Available in Your County

The standard Part B premium amount is set by Medicare and applies nationwide. What varies dramatically by ZIP code are the Medicare options available to you and the extent to which they can help minimize your Part B costs.

Here’s what veterans don’t realize: Your neighbor two counties over may have completely different options than you do. What worked for your military buddy in another state may not even exist where you live. And even if the same option is available in your area, what’s right for him may not be right for you. Different VA benefits, whether or not you have TRICARE for Life, different healthcare needs, all require different solutions.

Veterans in neighboring counties often have access to vastly different options with dramatically different opportunities to minimize Part B costs. A solution that works in one ZIP code may not even exist in the next.

Step 3 – Evaluate Total Value

Minimizing your Part B costs isn’t the only factor to consider. You need to evaluate the complete package.

Look at the provider network, especially if you travel. Review what additional benefits may be included with the option. Check prescription drug coverage if you don’t rely entirely on VA or TRICARE for Life. Most importantly, understand how the option works alongside your VA benefits or TRICARE for Life.

The right choice depends on your specific situation, not just which option offers the greatest Part B cost savings.

Step 4 – Enroll During Appropriate Periods

You can enroll during:

- Your Initial Enrollment Period around your 65th birthday

- The Annual Election Period (October 15 through December 7)

- The Medicare Advantage Open Enrollment Period (January 1 through March 31) if you’re already enrolled and want to switch

- Special Enrollment Periods after certain qualifying life events

Don’t confuse the Medicare Advantage Open Enrollment Period with the General Enrollment Period, which also runs January 1 through March 31 but serves a completely different purpose for initial Medicare enrollment if you missed your Initial Enrollment Period.

Missing these windows means waiting months for the next opportunity. Timing matters.

Step 5 – Understand Your Billing

If you enroll in an option that helps minimize your Part B costs, changes typically take effect one to three billing cycles after your option becomes active. If Social Security deducts your Part B premium, you’ll see the adjustment in your monthly benefit. If you pay Medicare directly, your quarterly bill will reflect any changes.

The enrollment process takes 30 to 45 minutes online. Finding the option that best fits your specific situation takes considerably longer because you’re comparing multiple options across different insurance companies, all with different benefits and varying degrees of Part B cost assistance based on your ZIP code.

6. Why Independent Veteran-Focused Specialists Matter

Working with independent specialists who focus exclusively on veterans helps ensure you’re not overpaying for Medicare Part B. The difference isn’t just about finding an option that helps with Part B costs. It’s about finding the option that best fits your complete situation as a veteran.

The Problem with Limited Access

Many veterans don’t realize that Medicare advisors are often tied to specific insurance companies or limited in what they can offer. Advisors working for specific companies face built-in constraints.

They can only show you their company’s options. They’re trained only on their employer’s products. They may not know about other options from different companies. Company priorities can influence their recommendations.

Generic Medicare advisors face additional limitations. They often don’t know which options work best alongside VA or TRICARE for Life benefits. They frequently overlook regional insurers that may offer better value in your specific area. They treat you like every other 65-year-old instead of recognizing your veteran-specific situation.

True Independence Makes a Difference

As independent specialists focusing exclusively on veterans, we evaluate all available options in your area, not just the popular ones. We have no corporate pressure to recommend specific options. We work for you, not an insurance company.

Medicare compensation rules mean we receive the same payment regardless of which option you choose. This removes any financial incentive to steer you toward one option over another. Your decision is based purely on what works best for your situation.

Our standard is simple. We never recommend a product that we wouldn’t recommend to our own parents if they lived in your ZIP code and county and had your same needs. This isn’t just a nice saying. It’s how we operate every single day.

Our Specialized Tools Make the Difference

My team and I have developed proprietary systems to filter Medicare data instantly, identifying opportunities to avoid overpaying for Part B and finding options with the most comprehensive benefits in your area within moments. These specialized tools we’ve created specifically for veteran Medicare analysis allow us to accomplish in minutes what might take you hours or days. We understand which insurance companies specifically value veteran enrollment and know how to analyze options based on your existing military benefits.

Veteran-Specific Knowledge Matters

Understanding how Medicare works alongside VA benefits and TRICARE for Life requires specialized knowledge. Generic advisors may not understand these interactions. We’ve spent years working exclusively with veterans, learning which options integrate best with military benefits.

We understand which insurance companies value veteran enrollment and structure their benefits accordingly. We know how to evaluate options based on your existing military healthcare coverage. This specialization consistently results in better outcomes for veterans because we’re not treating you like a generic Medicare beneficiary.

The Cost of Working with Us

Medicare rules allow us to provide all services completely free to veterans. Your Medicare coverage costs exactly the same whether you work with us or go directly to insurance companies. The difference is you get veteran-focused guidance at no additional cost to you.

7. Common Misconceptions That Cost Veterans Money

- Common Misconceptions That Cost Veterans Money

Over the years, I’ve heard every concern about minimizing Part B costs through Medicare options. Most come from misinformation or generic Medicare advice that doesn’t account for veteran benefits.

Myth – “Options that help with Part B will interfere with my VA care”

Reality – Medicare options from private companies operate completely independently from VA benefits. You continue using VA facilities exactly as before while accessing your Medicare Part B coverage, getting your Part B premiums as low as possible, and accessing additional benefits that VA, Medicare, and TRICARE for Life don’t offer. The two systems don’t interfere with each other.

Myth – “TRICARE for Life won’t work with these options”

Reality – TRICARE for Life works alongside these Medicare options as wraparound coverage, paying your deductibles, copays, and coinsurance for covered medical services. Your TFL coverage continues exactly as before.

Myth – “If it sounds too good to be true, it probably is”

Reality – Options that help veterans avoid overpaying for Part B are legitimate Medicare benefits regulated by the Centers for Medicare & Medicaid Services. They’re not promotional offers that disappear. Paying less for Part B isn’t “too good to be true” when you’ve already paid tens of thousands of dollars in Medicare taxes over your working career. You earned these benefits through FICA contributions your entire working life.

Myth – “I’ll lose my low costs if I travel”

Reality – Many options have nationwide PPO networks. Most veterans who work with specialists choose PPO options for this flexibility. Even HMO options provide emergency coverage at any hospital in the country.

Myth – “The insurance company can cancel my benefits anytime”

Reality – Options must maintain their benefits for the entire calendar year. Changes can only be made for the following year and must be approved by Medicare. Your benefits remain stable for the full year once you enroll.

Every year during the Annual Election Period from October 15 through December 7, you can evaluate all available options in your area and switch to whichever one best fits your current needs. This gives you the opportunity to ensure you’re always in the best option available.

Another advantage these Medicare options offer is that they cannot use medical underwriting to deny you coverage during enrollment periods. Unlike other Medicare coverage options that can reject you or charge higher premiums based on your health conditions, these options must accept you regardless of your health status as long as you are enrolled in Medicare Part A and B.

8. Strategic Considerations for Different Types of Veterans

Every veteran’s situation is unique. Your optimal strategy depends on your specific circumstances, existing military benefits, and healthcare preferences.

VA-Primary Users

If you receive most of your care through the VA, focus on options that minimize your Part B costs since you’ll use Medicare benefits less frequently. Look for nationwide PPO networks that give you flexibility for both emergency and non-emergency care anywhere in the country. For example, if you want to see a renowned specialist for a knee replacement in another state, or simply prefer a particular surgeon your buddy recommended, a PPO option lets you do that. Remember, whether you choose a PPO or HMO option, you’re always covered for emergency services nationwide without any network restrictions. When you primarily use the VA, keeping your Part B costs as low as possible means more money stays in your pocket, but you still have nationwide access whenever you need or want it.

TRICARE for Life Users

Since TFL covers out-of-pocket costs, keeping your Part B premiums as low as possible means more money stays in your pocket. Focus on options that are allowed to minimize your Part B premiums and provide PPO networks with nationwide coverage. Remember that PPO options provide out-of-network coverage too, and TFL still pays those deductibles, copays, and coinsurance. This combination gives you incredible flexibility while maintaining cost protection.

Don’t forget about additional benefits that VA, Medicare, and TFL don’t provide. These additional benefits enhance your coverage without affecting your low Part B premiums.

High-Income Veterans (IRMAA Payers)

If you pay higher Part B premiums due to Income Related Monthly Adjustment Amounts (IRMAA), finding options where your Part B premiums are as low as possible becomes even more important. For example, if your 2023 income puts you in the first IRMAA bracket, you pay $259 monthly instead of the standard $185. Minimizing your Part B premiums provides significant relief when you’re already paying elevated amounts.

Many veterans can appeal IRMAA surcharges if their income has dropped due to retirement or other life-changing events. Visit our IRMAA information page at https://veteransadvantagefinancial.vet/irmaa/ or download Form SSA-44 directly at https://www.ssa.gov/forms/ssa-44.pdf.

Frequent Travelers

Look for options combining nationwide PPO networks that keep your Part B premiums as low as possible. This combination provides coverage flexibility while minimizing what you pay for Part B. Pay attention to emergency coverage provisions and urgent care coverage while traveling. Remember, whether you have an HMO or PPO option, emergency care is always covered nationwide without any network restrictions. The key difference is that PPO options also give you the freedom to see providers outside of your network for non-emergency care while you’re traveling, not just emergencies.

9. Key Takeaways for Veterans

✓ Options that minimize Part B costs are legitimate Medicare benefits regulated by CMS, not promotional gimmicks

✓ Veterans may have additional options available because their existing benefits can affect how insurance companies assess coverage needs

✓ The Medicare options available to veterans differ significantly based on ZIP code and county

✓ Independent veteran specialists evaluate all available options because they’re not limited by company ties or quotas

✓ Paying less for Part B compounds over time. Keeping premiums as low as possible throughout retirement adds up significantly

✓ Medicare options don’t interfere with existing benefits. VA care, TRICARE for Life, and military benefits continue unchanged

✓ Annual reviews ensure you’re in the best available option. What’s available and premiums change each year

10. What’s Coming Next

You now understand one of the most valuable but underutilized benefits available to veterans: accessing the lowest possible Part B premiums through Medicare options from private companies. When combined with your existing VA or TRICARE benefits, keeping your Part B costs as low as possible means more money stays in your pocket while providing additional coverage that Original Medicare doesn’t offer.

In Chapter 6, we’ll tackle the other side of the Medicare financial equation: avoiding the costly penalties that can drain your retirement income for decades. You’ll discover why the dangerous myth that “VA coverage protects you from penalties” costs veterans thousands, learn exactly when you must enroll in Medicare, and understand how military retirees can lose both TRICARE for Life AND face lifetime penalties.

Most importantly, you’ll learn how to protect yourself from penalties that grow every year with Medicare premium increases, and how to appeal if you’ve been incorrectly charged. The next chapter could save you from financial mistakes that compound into tens of thousands of dollars over retirement.

Ready to find out what options are available in your area to keep your Part B premiums as low as possible? My team and I specialize exclusively in helping veterans avoid overpaying for Medicare. Call us at 888-960-8387 (VETS) for a free, personalized review of the Medicare options available in your specific area. Experience what WE SPEAK VETERAN™ really means.

Chapter 6 — Avoiding Medicare Penalties

How to keep your hard-earned dollars instead of paying Uncle Sam for life

1. Why Medicare Penalties Exist (And Why They’re So Brutal)

Let me start with a story that illustrates exactly what my team and I see regularly. After nearly 20 years in the Medicare industry, now specializing exclusively with veterans, I’ve seen this costly mistake too many times. A Navy veteran had delayed enrolling in Medicare Part B for three years because he thought his VA coverage was sufficient. When he finally came to us, he was facing a 30% lifetime penalty on his Part B premium.

Instead of paying the standard $185 monthly, he now pays $240.50 every month for 2025. This includes the 30% penalty. What makes this penalty especially brutal is that it’s calculated as a percentage of the current year’s Part B premium, not a fixed dollar amount. This means as Medicare premiums rise every year, your penalty grows right along with them. This penalty lasts for the rest of his life. Over 20 years, that’s at least an extra $13,320, assuming the Part B premium never increases. But we know it will increase, making the actual cost much higher.

Congress didn’t create Medicare penalties to be cruel. They created them to prevent what insurance companies call “adverse selection.” Without penalties, healthy people would wait until they got sick to enroll in Medicare, leaving only the sickest people in the program. This would drive costs through the roof for everyone.

The penalty system creates a powerful incentive. Enroll when you’re supposed to, and you pay standard rates. Wait until you’re sick, and you pay extra for the rest of your life. It’s harsh, but it keeps the entire Medicare system as financially stable as possible.

The Three Types of Medicare Penalties:

- Part B Late Enrollment Penalty: 10% per year you delay, permanent

- Part D Late Enrollment Penalty: 1% per month you delay, permanent

- Part A Late Enrollment Penalty: 10% for twice the delay period (only affects those who must buy Part A)

For veterans, the Part B penalty is by far the most dangerous because VA benefits are not creditable coverage for Medicare Part B, meaning you can’t use VA healthcare to justify delaying Medicare enrollment.

This is often confused with VA drug coverage, which is creditable for Part D penalties. VA and TRICARE for Life prescription coverage protects you from Part D penalties, but they do not protect you from Part B penalties. During my extensive time helping veterans navigate Medicare, this confusion between VA drug coverage being creditable and VA medical coverage not being creditable has cost more veterans money than almost any other misconception.

2. The Part B Penalty: Simple Math, Devastating Results

The Part B late enrollment penalty is brutally simple to calculate but devastating in its long-term impact. Throughout my Medicare career working with veterans, I’ve seen how this simple formula can cost tens of thousands of dollars.

The Formula:

- 10% penalty for every full 12-month period you delay enrollment

- Applied to the current year’s Part B premium (not a fixed dollar amount)

- The penalty lasts for as long as you have Medicare Part B, typically for life

As I explained earlier, your penalty grows every year along with Medicare premiums. Let me show you what this means using conservative projections.

If You Should Enroll in 2025 But Delay 3 Years Until 2028:

- 2025: You miss enrollment (standard premium $185)

- 2028: You finally enroll with 30% penalty. Your premium: $276.80 (penalty: $63.88)

- 2030: Your premium grows to $350.70 (penalty: $116.90)

The Compounding Effect: Assuming just a 4.8% annual increase in Part B premiums, your penalty burden grows significantly:

- 1 year delay (10% penalty): Start paying $19.39 extra monthly, grows to $23+ by 2030

- 3 years delay (30% penalty): Start paying $63.88 extra monthly, grows to $117+ by 2030

- 5 years delay (50% penalty): Start paying $116.90 extra monthly, grows to $175+ by 2030

A 3-year delay from your 2025 enrollment date doesn’t just cost you $64 extra per month initially. That penalty grows every single year for the rest of your life. Looking at the projections, a veteran who delays 3 years will pay over $89 monthly in penalties by 2029 and over $116 by 2030.

Over 20 years, you’re looking at paying at least $20,000-$25,000 extra in penalties alone, and that’s assuming premium increases stay modest at 4.8% annually. For veterans on fixed incomes combining Social Security and military retirement, this unnecessary expense can significantly impact retirement security.

Year Enrolled | Years Delayed | Estimated Part B Premium | Penalty (10% per year) | Total Monthly Premium |

2025 | 0 | $185.00 | $0 | $185.00 |

2026 | 1 | $193.88 | $19.39 | $213.27 |

2027 | 2 | $203.18 | $40.64 | $243.82 |

2028 | 3 | $212.92 | $63.88 | $276.80 |

2029 | 4 | $223.12 | $89.25 | $312.37 |

2030 | 5 | $233.80 | $116.90 | $350.70 |

3. The Dangerous Myth: “VA Coverage Protects Me”

During my extensive Medicare career, now dedicated entirely to veterans, I’ve discovered that this single misunderstanding costs more money than almost any other Medicare mistake. Unlike group health insurance through a large employer, VA benefits are not creditable coverage for Medicare purposes.

The Social Security Administration recognizes specific types of creditable coverage that allow you to delay Part B without penalty:

Approved Creditable Coverage:

- ✓ Employer group health plan with 20+ employees (while actively working)

- ✓ Federal Employees Health Benefits (FEHB) (while actively working; retirees must enroll in Part B to avoid penalties)

- ✓ A spouse’s large employer coverage (while they’re actively working)

- ✓ Some union health plans with specific characteristics

NOT Creditable Coverage:

- ✗ VA health care (all types and priority groups)

- ✗ VA Community Care

- ✗ CHAMPVA

- ✗ COBRA coverage

- ✗ Most retiree health plans

- ✗ Individual/private insurance policies

- ✗ Medicaid

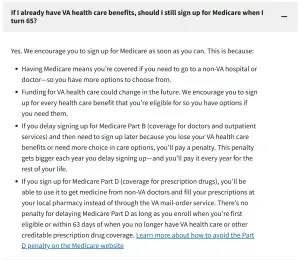

The VA’s Own Warning: “Yes. We encourage you to sign up for Medicare as soon as you can. This is because:

- Having Medicare means you’re covered if you need to go to a non-VA hospital or doctor, so you have more options to choose from.

- Funding for VA health care could change in the future. We encourage you to sign up for every health care benefit that you’re eligible for so you have options if you need them.

- If you delay signing up for Medicare Part B (coverage for doctors and outpatient services) and then need to sign up later because you lose your VA health care benefits or need more choice in care options, you’ll pay a penalty.”